million b/d Shell share

[A] Subject to successful completion of

announced deals.

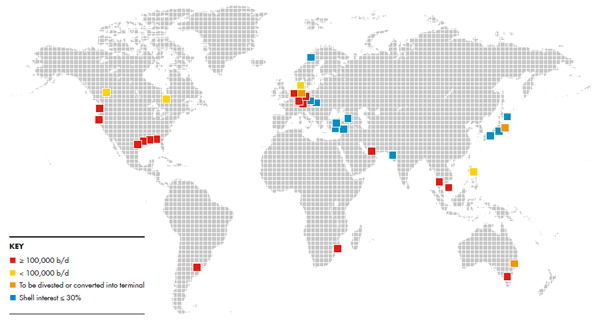

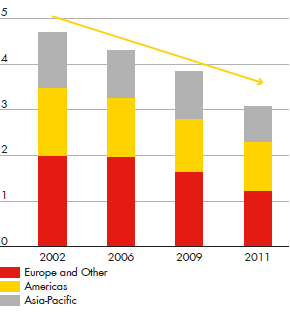

We have interests in more than 30 refining sites worldwide. Together, they processed 2.8 million barrels of crude oil a day in 2011 into a wide range of products, including gasoline, diesel, heating oil, aviation fuel, marine fuel, lubricants, liquefied petroleum gas, sulphur and bitumen. Around 35% of our refining capacity is in Europe, 30% in the Americas and 30% in Asia-Pacific.

We focus on energy-efficiency improvements at our refineries and chemicals plants. Those improvements have contributed to a reduction in their greenhouse gas emissions. Achieving even greater efficiency will help us deliver more profitability – so too will greater operational reliability. The average availability of our refineries – a measure of their operational excellence – was 92% in 2011.

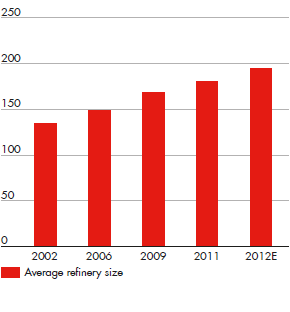

A key part of our strategy is to divest non-core assets while selectively investing in high-growth markets, especially in the East. We aim to create a Downstream portfolio that is more focused on larger, integrated refining sites that are better able to respond to tighter fuel specifications and growth opportunities.

The Port Arthur refinery in Texas, USA, will have a prominent place in that portfolio. Part of the joint venture Motiva Enterprises (Shell interest 50%) is currently in the finishing stages of an expansion project that will make it the largest refinery in our portfolio. The expanded refinery will have a total capacity of some 600 thousand b/d and be capable of handling most grades of crude oil. New technology will also lower most emissions from the refinery on a per-barrel basis.

Including the Port Arthur expansion, we have reduced our refining capacity by 15% between 2009 and 2012. The capacity reduction amounts to around 800 thousand b/d, most of it located in Europe, where the market has been in oversupply. Since 2002, capacity has been reduced by around a third. We have retained the larger and more integrated refineries and petrochemical plants, and the current portfolio is positioned for optimisation across the entire value chain. Major asset sales have been completed, but we will continue to review the portfolio regularly and improve it further where necessary.