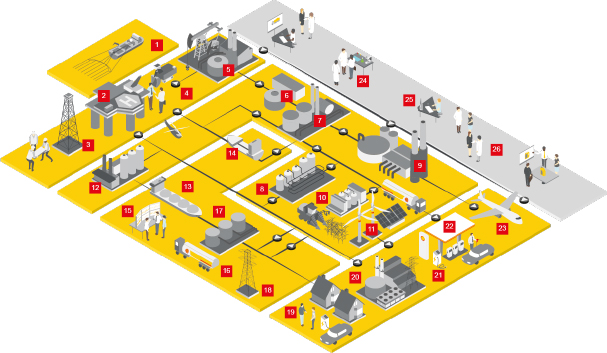

Taxation of our businesses

Our tax data reflect the varied nature of our activities. We have a large portfolio of assets and businesses in different countries and at different stages of the business cycle, from start-up to decommissioning. The business model, the stage in the investment cycle and business performance drive much of our taxes paid.

Our business profits are closely linked to oil and gas prices and so are our taxes. When oil prices are higher, we see a greater proportion of profits being taxed at higher upstream tax rates. When oil prices are lower, a lower overall effective tax rate (ETR) might be expected. While average oil and gas industry prices in 2020 were lower than in 2019, Shell’s ETR in 2020 was primarily influenced by asset impairments. Further details on our ETR can be found in the Annual Report and Accounts 2020.

The Upstream and Integrated Gas businesses generate a significant part of our taxation charge. Governments often have specific oil and gas fiscal regimes with tax rates that are higher than those for other industries. Upstream and Integrated Gas projects have phases and our total tax fluctuates depending on the phase of a project.

Our contributions to a country are not always included in the corporate income taxes reported. We may have agreed with governments to make payments as a share of the oil and gas we produce, through royalties or indirect taxes. Details of these payments are included in our Payments to Governments Report.

Downstream includes the business activities for manufacturing and energy production, chemicals, transport and trading, and sales and marketing. These activities are usually taxed at a country’s standard rate of corporate income tax. Downstream tax contributions are mainly driven by our physical presence in countries where we have refineries, chemical plants and retail sites.

In addition to corporate income taxes, we pay import and export duties and other tariffs on our transport and trading activities. Our Retail business handles large volumes of sales transactions, which incur consumption taxes and fuel duties. These are collected and paid to the authorities.

Manufacturing and energy production require a significant number of employees working in plants and refineries, raising revenues for governments through employment taxes.

Companies in Projects & Technology pay taxes in the countries where they reside. The service fees they charge are typically tax deductible for the recipient as business costs, following local tax principles and rules.

Corporate covers the non-operating activities and central functions that support our businesses. The majority of the costs related to our headquarters and central functions are recovered from the business segments. Those costs that are not recovered are retained in Corporate. See Supporting services for more detail.